What’s Next for Inflation? 4 Things Skilled Trades Pros Need to Know

Key Takeaways:

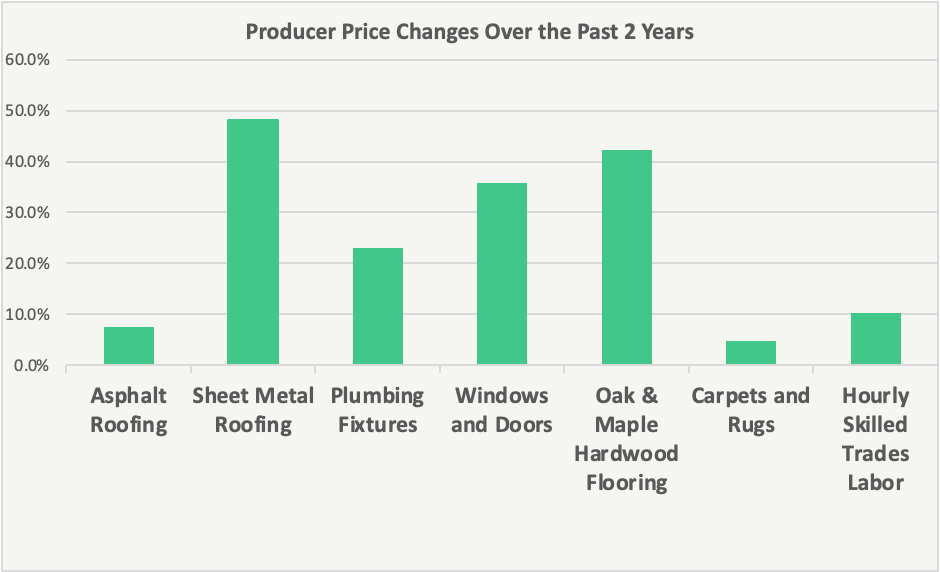

- Inflation varies a lot depending on the product, even with the same category of projects. For example, since the onset of the pandemic asphalt shingle prices have increased 8%, while sheet metal roofing prices have increased 48%.

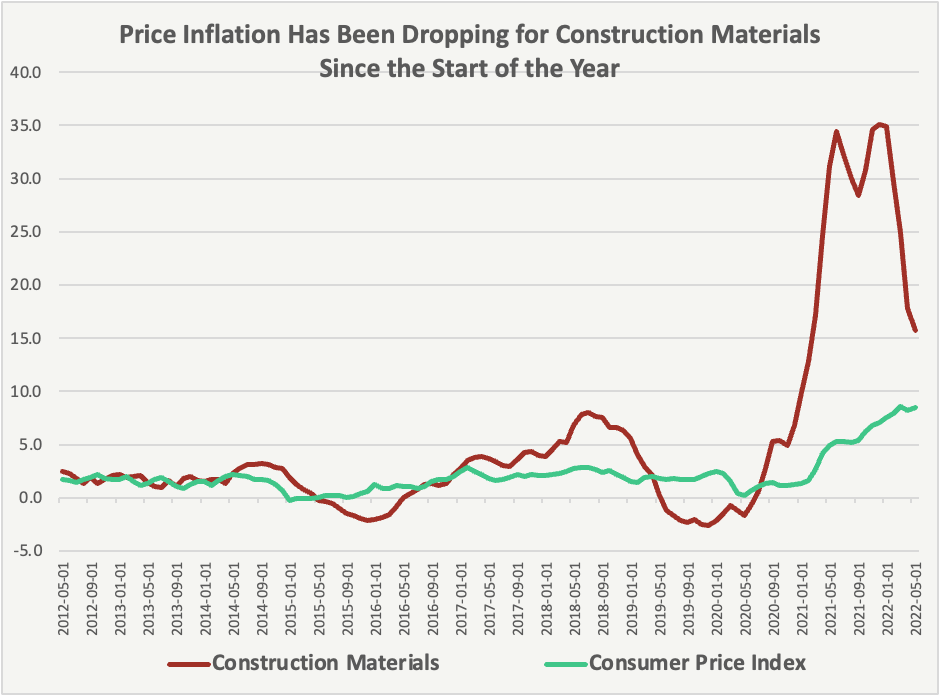

- Inflation for construction materials has already begun declining, dropping from 35% in January to 16% in May.

- Extrapolating from basic consumer expectations suggests overall inflation will drop to the 5-6% range one year from now, but macroeconomic uncertainty limits the confidence in most forecasts.

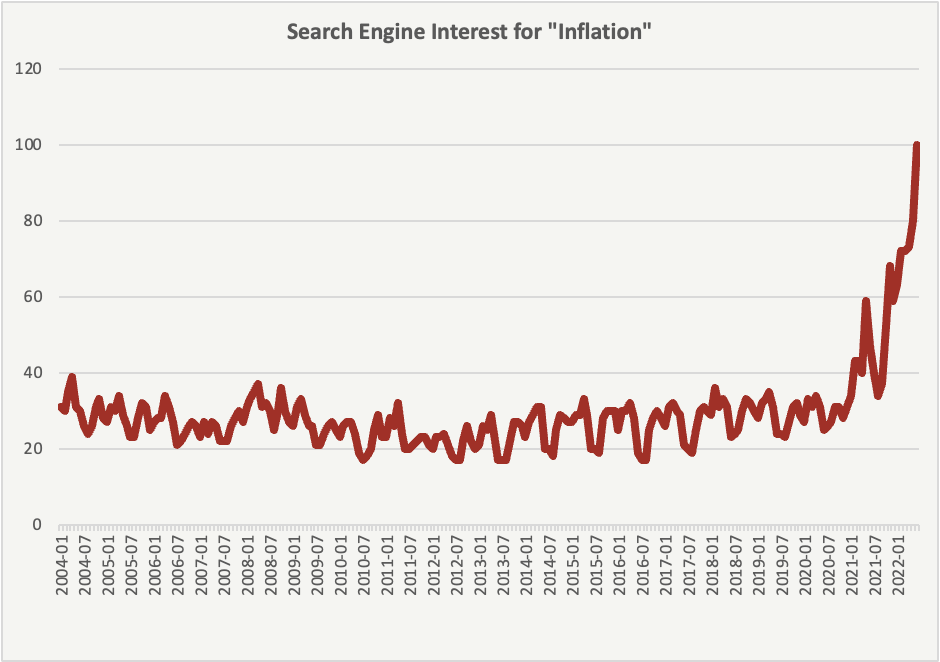

Inflation has been top of mind after reaching a multi decade high. Inflation can erode the buying power of both consumers and businesses, and can be a source of anxiety and worry for many. It can also be detrimental to businesses’ operating margins and personal household financial planning if not properly accounted for, so here are 4 things you should know going forward.

1. “Inflation is not a one size fits all number

Describing inflation as a single number is great for straightforward communication of the basic concept, but if you are relying on the single number for your own planning, you risk eroding your margins.

That is because changes in cost are different across different categories. Not only does this mean flooring and roofing prices might be changing at different rates, but that even within a category like roofing there are potentially large changes in price. For example, since the onset of the pandemic, asphalt roofing prices have risen by roughly 10%, while sheet metal roofing producer prices have increased nearly 5 times that amount.

2. Inflation has already peaked for construction materials

Looking at the broader index of construction materials, the inflation rate has already dropped by half, falling from 35% at the start of the year to 16% in the latest data.

If the trend continues, the series could reach its historical rate by the end of the summer.

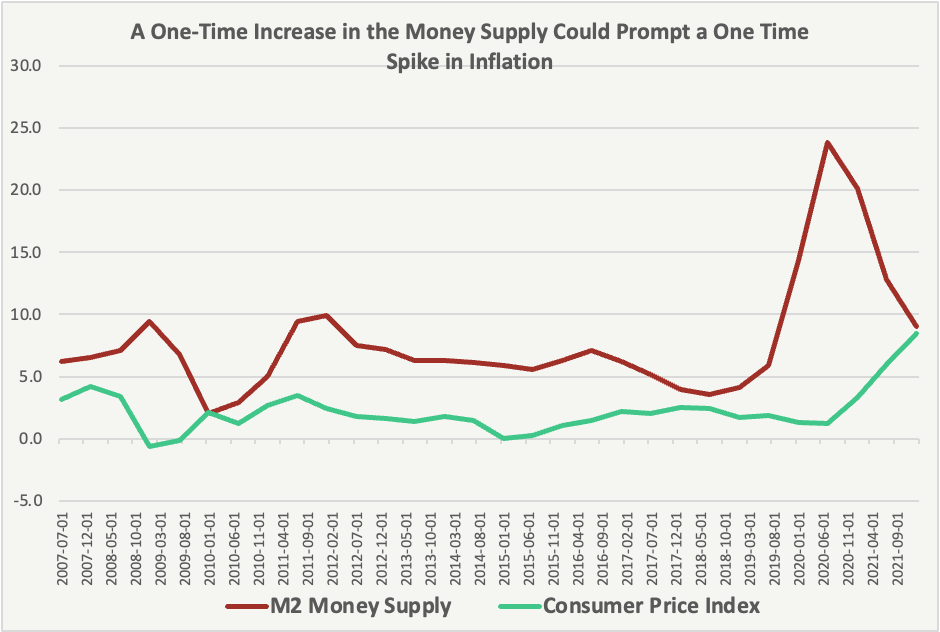

3. Monetary inflation should be a one-time event

Some of the focus around inflation has been the role of the amount of money in circulation following economic stimulus efforts to combat the pandemic.

Sidestepping a century long debate among economists about the relationship between inflation and the money supply, to note that a large one-time increase in the supply of money should result in a single increase in the price level. Looking at the relationship between the change in the M2 money supply and a change in the Consumer price Index shows that under this scenario we are partially through some of this effect

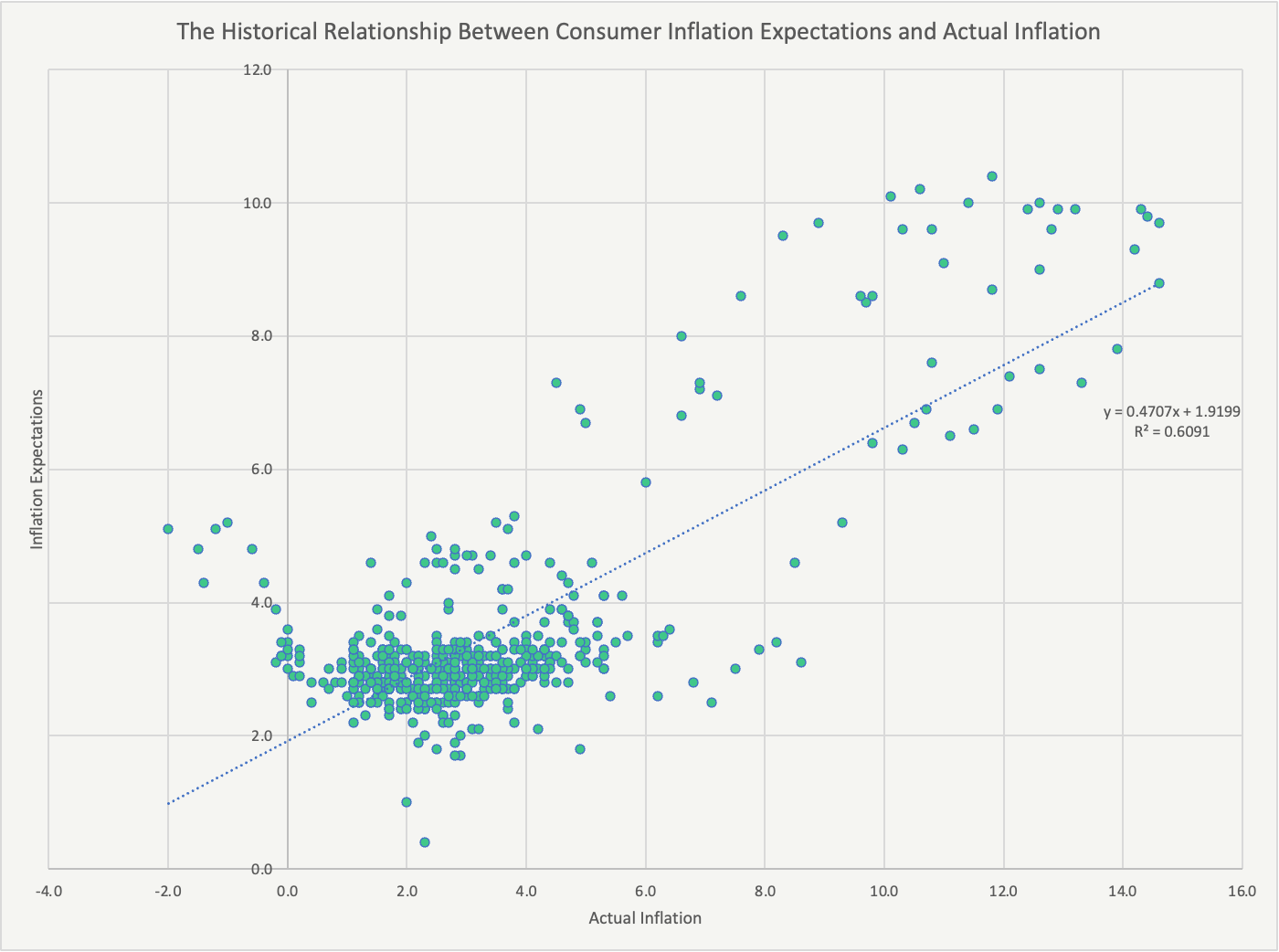

4. But… inflationary expectations can have their own momentum

Countering this one-time adjustment effect, is the competing concern unique to inflation is that it can develop its own momentum.

This is because businesses expect their input costs to rise so they raise their prices in advance, while consumers in turn expect higher prices for the goods and services they expect to consume from businesses and ask for higher salaries in anticipation. This creates a feedback loop of higher prices and higher wages that can generate its own momentum.

Looking at the historical correlation between consumer inflation expectations and actual inflation one year later suggests that inflation could be around 5-6% one year from now.

Summary

Inflation carries risks to your bottom line as a business, or your household financial planning as a consumer. As you plan for the second half of 2022, remember that there’s a wide variety in price changes taking place right now, the rate of increase is already dropping in construction materials, inflation from extra money circulating in the economy should be a one-time event, but inflationary expectations can have their own momentum and that momentum suggests we could still have 5% inflation a year from now based on past observations about consumer expectations.

Methodology

The underlying price data in this research note comes from the Bureau of Labor Statistics producer price indices. Actual market prices vary from the indices, to read more background on producer price indexes and how they differ from consumer prices, you can read here: https://www.bls.gov/ppi/faqs/questions-and-answers.htm

Press & Media Inquiries

Press & Media Inquiries Angi Economics

Angi Economics